|

Analysis of $traight’s Tax Records: a hundred million dollar charity for white kids only |

|

|

Analysis of $traight’s Tax Records: a hundred million dollar charity for white kids only |

|

by Wes Fager (c) 2000

|

|

|

| There are four tables in this section: | |

| Table 1 | shows IRS 990 tax forms for Straights. From time-to-time we will add hyperlinks to those forms which we have. |

| Table 2 | gives the combined total income and expenses for Straight, Inc. plus Straight Foundation, Inc. for the periods 1983 - 1995. It combines the data of Table 3 and Table 4. |

| Table 3 | gives a breakdown of incomes and expenses for Straight, Inc.-only from 1983 to 1993. |

| Table 4 | gives a breakdown of income and expenses for Straight Foundation, Inc.-only from 1985 - 1995. |

|

The first-time reader should probably just look at these tables to gain insight into the magnitude of the sums of money involved and to see the types of things the Straights claimed as income and the types of things it declared as expenses. Following the tables is a lengthy analysis of certain items of income and expense which the Straight's declared. Straight, Inc. was founded in 1976 and changed its name and mission to Straight Foundation, Inc. in 1985 at which time a new juvenile drug treatment program called Straight, Inc. was created which operated until 1993. In 1996 Straight Foundation, Inc. changed its name again to its current name--the Drug Free America Foundation, Inc. Being tax exempt charities the tax records for both Straight, Inc. and Straight Foundation, Inc. are open for public inspection. Tax exempt organizations like Straight are required to file taxes on an IRS Form 990. Table 1 gives the Form 990's for which I have records. I have included hyperlinks for some of them. Raw data from these forms is used to build Tables 2, 3 and 4. Straight's fiscal year begins on October 1, thus the IRS 990 Form for 1988, for example, gives Straight's tax record for the period October 1, 1988 through September 30, 1989. As you can see I do not have filings for Straight Inc. from 1976 to 1982, and for 1992. Nor do I have filings for Straight Foundation, Inc. for 1992, 1994 and 1996 to 2000. However, Schedule A to the 19XX return in later years gives incomes for the previous 4 years thus I have the income-only part of Straight, Inc. and Straight Foundation, Inc. for 1992, and the income-only part of Straight Foundation, Inc. for 1994.

|

|

.

| Table 2 below gives Total Incomes & Expenses for Straight, Inc. and Straight Foundation, Inc. Combined. Table 2 combines the incomes and expenses from Tables 3 and 4 giving separate total columns from 1983 - 1991 (because I have un-interrupted records for these years), and from 1983 - 1995 (as best as can be done since expenses for 1992 and 1994 are not known). From 1983 to 1995 Straight, Inc. and Straight Foundation, Inc. combined claimed to have taken in $87 million, but they spent over $86 million operating the program. Later in the analysis portion of this study, we will see why a truer picture is that the Straight's grossed nearly a hundred million dollars. As noted on the spread sheet, a truer figure for total expenses (assuming $2.5 million for operating expenses in 1992) would be $88.5 million in total expenses resulting in a net deficit of $1.5 million between 1983 and 1995. In other words Straight's records would seem to indicate that though they grossed $87 million, they actually lost over a million dollars doing their charitable work. As you will see from the table, some of the major expenses include: |

| $44 million | for salaries (non-fundraising and fundraising) |

| $10 million | in bad debts (where parent did not pay up) |

| $11 million | for rent and rental expenses. (Beyond this $11 million, Straight Foundation, Inc. rented properties to Straight, Inc. I did not include this rent in the total because I treated it as a wash.) |

| $3.5 million | for fund raising prizes |

| $2.3 million | for outside services |

| $2 million | for food |

| $1.3 million | for specific charitable assistance to individuals |

| $1.3 million | for miscellaneous. |

Table 2. Combined Income & Expenses for Straight, Inc. & Straight Foundation, Inc. 1983 - 1995

|

Combined Incomes |

Combined Incomes |

|||||

|

Straight, Inc. + |

Straight, Inc. + |

Straight, Inc. |

Straight, Inc. |

Straight Fdn, Inc. |

Straight Fdn, Inc. |

|

|

Straight Fdn, Inc. |

Straight Fdn, Inc. |

Income & Expenses |

Income & Expenses |

Income & Expenses |

Income & Expenses |

|

|

1983 - 1995 |

1983 - 1991 |

1983 - 1993 |

1983 - 1991 |

1985 - 1995 |

1985-1991 |

|

|

INCOME |

||||||

|

revenues (from program fees) |

$67,273,159 |

$66,621,078 |

$67,159,675 |

$66,621,078 |

$113,484 |

$0 |

|

income from grants |

||||||

|

from Straight Foundation |

$3,280,747 |

$2,724,249 |

||||

|

from direct public support |

$18,029,189 |

$17,219,479 |

$15,759,256 |

$15,208,118 |

$2,269,933 |

$2,011,361 |

|

rentals |

$4,354,800 |

$4,354,800 |

||||

|

other |

$1,722,835 |

$554,734 |

$1,458,731 |

$354,040 |

$264,104 |

$200,694 |

|

------------------- |

------------------- |

------------------- |

------------------- |

------------------- |

------------------- |

|

|

Total Income 1983 - 1995 |

$87,025,183 |

$84,395,291 |

$87,658,409 |

$84,907,485 |

$7,002,321 |

$6,566,855 |

|

EXPENSES |

||||||

|

grants to Straight, Inc. |

$3,280,747 |

$2,724,249 |

||||

|

grants to non-Straights |

$58,000 |

$0 |

$58,000 |

$0 |

||

|

wages & payroll taxes |

||||||

|

non fundraising |

$42,885,955 |

$42,885,955 |

$42,885,955 |

$42,885,955 |

$0 |

$0 |

|

rent |

$6,411,118 |

$6,411,118 |

$10,633,280 |

$10,633,280 |

$511 |

$511 |

|

rental expenses |

$4,358,938 |

$4,358,938 |

$4,358,938 |

$4,358,938 |

||

|

bad debts |

$9,673,901 |

$9,673,901 |

$9,673,901 |

$9,673,901 |

0 |

$0 |

|

fundraising |

||||||

|

wages & payroll taxes |

$1,154,295 |

$1,154,295 |

$881,454 |

$881,454 |

$272,841 |

$272,841 |

|

prizes |

$3,457,720 |

$3,457,720 |

$3,457,720 |

$3,457,720 |

0 |

$0 |

|

rent |

$132,127 |

$132,127 |

$0 |

$0 |

||

|

printing |

$76,414 |

$76,414 |

$76,414 |

$76,414 |

||

|

other fundraising |

$107,298 |

$107,298 |

$107,298 |

$107,298 |

||

|

specific assistance to people |

$1,375,024 |

$1,375,024 |

$1,375,024 |

$1,375,024 |

$0 |

$0 |

|

legal fees |

$601,164 |

$582,470 |

$120,174 |

$108,599 |

$480,990 |

$473,871 |

|

printing |

$1,215,430 |

$1,215,430 |

$1,215,430 |

$1,215,430 |

$0 |

$0 |

|

food |

$1,995,741 |

$1,995,741 |

$1,995,741 |

$1,995,741 |

$0 |

$0 |

|

insurance |

$375,108 |

$355,410 |

$166,701 |

$159,905 |

$208,407 |

$195,505 |

|

outside services |

||||||

|

service contracts |

$113,038 |

$113,038 |

$113,038 |

$113,038 |

$0 |

$0 |

|

medical services |

$314,095 |

$314,095 |

$314,095 |

$314,095 |

$0 |

$0 |

|

outside services |

$2,315,975 |

$2,315,975 |

$2,286,094 |

$2,286,094 |

$29,881 |

$29,881 |

|

miscellaneous |

$1,345,463 |

$1,345,463 |

$1,321,050 |

$1,321,050 |

$24,413 |

$24,413 |

|

other |

$8,289,055 |

$7,954,067 |

$7,912,528 |

$7,821,417 |

$376,527 |

$132,650 |

|

------------------- |

------------------- |

------------------- |

------------------- |

------------------- |

------------------- |

|

|

Total Expenses 1983 - 1995 |

$86,123,732 |

$82,054,048 |

$84,484,312 |

$84,374,830 |

$9,274,967 |

$8,396,571 |

Note: Total expenses for the period 1983 to 1995 is shown to be $86,123,732 but this does not include expenses for Straight, Inc. for the tax year 1992. Based on prior years a figure of $2.5 million is probably a good estimate. This assumption would lead to a deficit of (1,598,549) [$87,025,183 - ($86,123,732 + $2,500,000)]. Thus a reasonable estimate would show that Straight would claim that it had raised $87 million from 1983 to 1995, but its expenses had been $88.5 million producing a net loss of $1.5 million. [An assumed additional loss of another $50 - $60K for expenses from Straight Foundation, Inc. for expenses in 1992 and 1994 is not included.]

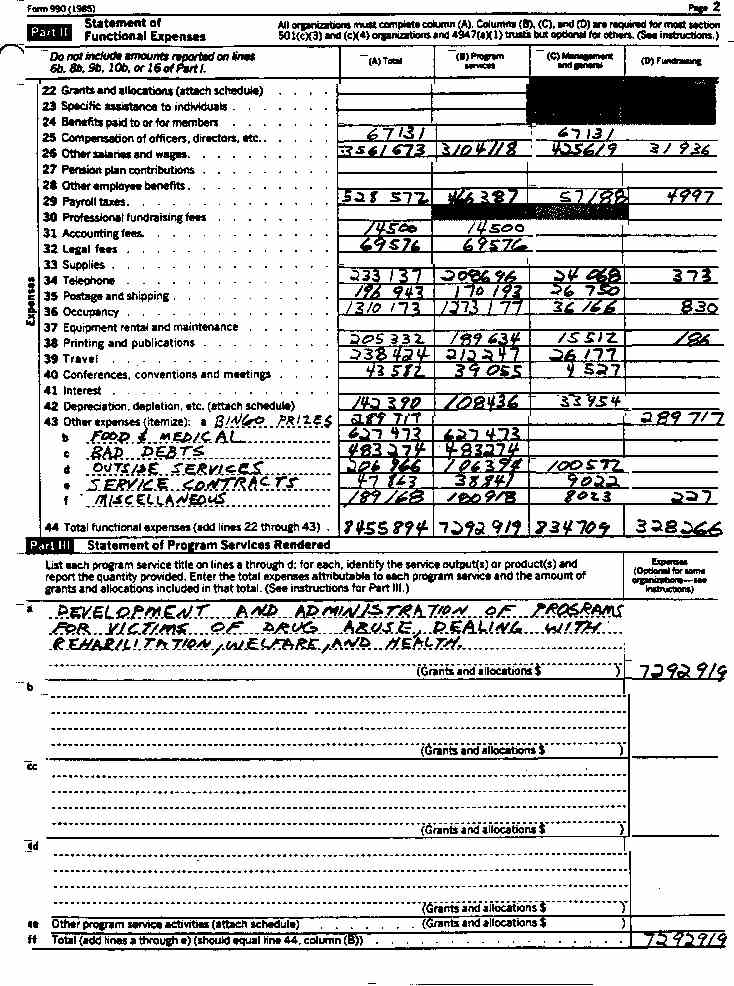

| Table 3: Straight, Inc. 1983 - 1995 (below) gives a detailed breakdown of incomes and expenses for Straight, Inc. by year from 1983 to 1993, plus two total columns. One total is for the years 1983 - 1991 because it is a complete spread sheet. The other total is for the years 1983 - 1993 realizing that the expense-only part of 1992 is not included. The bottom-line shows that according to its records, Straight, Inc. claims to have taken-in $87 million from 1983 - 1993 but had expenses of $84 million (not including expenses for 1992). Thus a net excess of $3 million. However, based on prior tax reportings, it would be reasonable to assume Straight, Inc.’s expenses for 1992 to be $2.5 million. Thus a truer figure for Straight, Inc.’s net excess/deficit for the period 1983 - 1993 is probably an excess of about $675,000. |

Table 3. Income & Expenses for Straight, Inc. 1983 - 1993

|

INCOME |

Tot 83 - 93 |

Tot 83 - 91 |

1993 |

1992 |

1991 |

1990 |

1989 |

1988 |

1987 |

INCOME |

1986 |

1985 |

1984 |

1983 |

|

|

donations & grants |

donations & grants |

||||||||||||||

|

from Straight Foundation |

$3,280,747 |

$2,724,249 |

556,498 |

0 |

0 |

150,000 |

534,817 |

0 |

242,421 |

from Straight Foundation |

541,292 |

1,255,719 |

0 |

0 |

|

|

from direct public support |

$15,759,256 |

$15,208,118 |

102,355 |

448,783 |

626,393 |

1,844,988 |

2,304,625 |

2,301,025 |

1,787,316 |

from direct public support |

2,084,371 |

958,791 |

1,774,268 |

1,526,341 |

|

|

revenues |

$67,159,675 |

$66,621,078 |

4,742 |

533,855 |

4,743,445 |

7,075,872 |

11,640,923 |

10,670,961 |

9,977,538 |

revenues |

10,000,495 |

5,962,099 |

3,885,385 |

2,664,360 |

|

|

interest |

$350,858 |

$350,858 |

0 |

0 |

1,436 |

6,698 |

31,611 |

70,819 |

35,529 |

interest |

11,525 |

28,179 |

84,764 |

80,297 |

|

|

forgiveness of bad debt |

$1,104,691 |

$0 |

0 |

1,104,691 |

0 |

0 |

0 |

0 |

0 |

forgiveness of bad debt |

0 |

0 |

0 |

0 |

|

|

other |

$3,182 |

$3,182 |

0 |

0 |

0 |

0 |

0 |

3,182 |

0 |

other |

0 |

0 |

0 |

0 |

|

|

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

|

--------------- |

--------------- |

--------------- |

--------------- |

||

|

TOTAL INCOME |

$87,658,409 |

$84,907,485 |

$663,595 |

$2,087,329 |

$5,371,274 |

$9,077,558 |

$14,511,976 |

$13,045,987 |

$12,042,804 |

TOTAL INCOME |

$12,637,683 |

$8,204,788 |

$5,744,417 |

$4,270,998 |

|

|

EXPENSES |

Tot 83 - 93 |

Tot 83 - 91 |

1993 |

1992 |

1991 |

1990 |

1989 |

1988 |

1987 |

EXPENSES |

1986 |

1985 |

1984 |

1983 |

|

|

wages, taxes, benefits |

wages, taxes, benefits |

||||||||||||||

|

program services |

$36,204,377 |

$36,204,377 |

0 |

2,128,599 |

4,295,660 |

7,221,529 |

5,733,770 |

4,432,078 |

program services |

5,137,503 |

3,570,505 |

2,148,208 |

1,536,525 |

||

|

management |

$6,450,409 |

$6,450,409 |

0 |

638,018 |

1,192,287 |

1,180,478 |

1,135,454 |

761,640 |

management |

543,816 |

482,807 |

319,120 |

196,789 |

||

|

officers & directors |

$231,169 |

$231,169 |

0 |

0 |

0 |

0 |

0 |

0 |

officers & directors |

0 |

67,131 |

83,413 |

80,625 |

||

|

fundraising |

fundraising |

||||||||||||||

|

wages & taxes |

$881,454 |

$881,454 |

0 |

167,359 |

178,986 |

275,561 |

178,171 |

0 |

wages & taxes |

0 |

36,933 |

27,276 |

17,168 |

||

|

rent |

$132,127 |

$132,127 |

0 |

6,784 |

12,702 |

25,890 |

22,980 |

19,950 |

rent |

24,405 |

830 |

18,586 |

0 |

||

|

bingo prizes |

$289,717 |

$289,717 |

0 |

0 |

0 |

0 |

0 |

0 |

bingo prizes |

0 |

289,717 |

0 |

0 |

||

|

prizes and awards |

$1,916,665 |

$1,916,665 |

0 |

72,885 |

525,058 |

734,471 |

584,251 |

0 |

prizes and awards |

0 |

0 |

0 |

0 |

||

|

miscellaneous (prizes?) |

$1,251,338 |

$1,251,338 |

0 |

0 |

4126 |

11,757 |

8,246 |

535,235 |

miscellaneous (prizes?) |

505,167 |

0 |

184,422 |

2,385 |

||

|

specific assist to people |

$1,375,024 |

$1,375,024 |

0 |

0 |

85,632 |

277,743 |

353,394 |

658,255 |

specific assist to people |

0 |

0 |

0 |

0 |

||

|

staff develop & education |

$110,771 |

$110,771 |

0 |

0 |

0 |

68,567 |

0 |

0 |

staff develop & education |

0 |

0 |

20,443 |

21,761 |

||

|

accounting fees |

$28,000 |

$28,000 |

0 |

13,500 |

0 |

0 |

0 |

accounting fees |

0 |

14,500 |

0 |

0 |

|||

|

legal fees |

$120,174 |

$108,599 |

11,575 |

39,023 |

0 |

0 |

0 |

0 |

legal fees |

0 |

69,576 |

0 |

0 |

||

|

supplies |

$1,111,694 |

$1,110,913 |

781 |

34,602 |

70,254 |

249,115 |

267,132 |

127,652 |

supplies |

229,232 |

0 |

86,739 |

46,187 |

||

|

telephone |

$804,627 |

$804,627 |

0 |

110,007 |

0 |

0 |

0 |

0 |

telephone |

262,950 |

233,137 |

112,941 |

85,592 |

||

|

postage |

$324,677 |

$324,557 |

120 |

32,778 |

0 |

0 |

0 |

46,115 |

postage |

0 |

196,943 |

31,792 |

16,929 |

||

|

1993 |

1992 |

1991 |

1990 |

1989 |

1988 |

1987 |

1986 |

1985 |

1984 |

1983 |

|||||

|

rent |

$10,633,280 |

$10,633,280 |

0 |

753,265 |

1,410,354 |

2,213,998 |

1,645,965 |

1,534,816 |

rent |

1,470,910 |

1,309,343 |

167,275 |

127,354 |

||

|

equipment rental & maint. |

$284,388 |

$284,388 |

0 |

50,730 |

69,794 |

45,319 |

50,860 |

31,612 |

equipment rental & maint |

36,073 |

0 |

0 |

0 |

||

|

printing |

$1,215,430 |

$1,215,430 |

0 |

48,895 |

72,523 |

342,510 |

268,621 |

7,613 |

printing |

33,471 |

205,332 |

153,345 |

83,120 |

||

|

travel & meetings |

$2,460,041 |

$2,460,041 |

0 |

89,579 |

289,095 |

455,773 |

590,443 |

214,562 |

travel & meetings |

316,727 |

282,006 |

157,388 |

64,468 |

||

|

interest |

$158,724 |

$158,724 |

0 |

0 |

0 |

0 |

0 |

0 |

interest |

0 |

0 |

98,267 |

60,457 |

||

|

depreciation |

$1,656,703 |

$1,656,703 |

0 |

191,751 |

209,626 |

237,222 |

185,852 |

140,374 |

depreciation |

177,491 |

142,390 |

206,031 |

165,966 |

||

|

food |

$1,995,741 |

$1,995,741 |

0 |

0 |

0 |

0 |

0 |

0 |

food |

620,551 |

602,407 |

381,071 |

391,712 |

||

|

medical |

$314,095 |

$314,095 |

0 |

0 |

0 |

0 |

0 |

0 |

medical |

266,593 |

25,066 |

15,856 |

6,580 |

||

|

bad debts |

$9,673,901 |

$9,673,901 |

0 |

1,233,266 |

1,763,753 |

752,819 |

1,405,644 |

1,485,142 |

bad debts |

1,996,739 |

483,274 |

347,561 |

205,703 |

||

|

loss contingencies |

$253,814 |

$253,814 |

0 |

17,740 |

13,031 |

3,647 |

28,521 |

0 |

loss contingencies |

0 |

0 |

0 |

190,875 |

||

|

insurance |

$166,701 |

$159,905 |

6,796 |

61,204 |

0 |

0 |

0 |

0 |

insurance |

0 |

0 |

52,080 |

46,621 |

||

|

outside services |

$2,286,094 |

$2,286,094 |

0 |

297,576 |

319,570 |

433,970 |

266,970 |

184,883 |

outside services |

220,160 |

206,966 |

230,946 |

125,053 |

||

|

service contracts |

$113,038 |

$113,038 |

0 |

0 |

0 |

0 |

0 |

0 |

service contracts |

47,863 |

35,294 |

29,881 |

|||

|

office |

$193,956 |

$193,956 |

0 |

0 |

0 |

0 |

0 |

0 |

office |

193,956 |

0 |

0 |

0 |

||

|

building maintenance |

$129,813 |

$129,813 |

0 |

0 |

0 |

0 |

0 |

0 |

building maintenance |

0 |

0 |

83,260 |

46,553 |

||

|

electric, water, sewage |

$275,611 |

$275,611 |

0 |

0 |

0 |

0 |

0 |

0 |

electric, water, sewage |

0 |

0 |

147,530 |

128,081 |

||

|

real estate taxes |

$29,499 |

$29,499 |

0 |

0 |

0 |

0 |

0 |

0 |

real estate taxes |

0 |

0 |

17,410 |

12,089 |

||

|

client refunds |

$90,210 |

$0 |

90,210 |

0 |

0 |

0 |

0 |

0 |

client refunds |

0 |

0 |

0 |

0 |

||

|

miscellaneous |

$1,321,050 |

$1,321,050 |

0 |

38,468 |

50,631 |

214,930 |

178,638 |

229,252 |

miscellaneous |

238,926 |

189,168 |

112,372 |

68,665 |

||

|

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

|

--------------- |

--------------- |

--------------- |

--------------- |

||

|

TOTAL EXPENSES |

$84,484,312 |

$84,374,830 |

$109,482 |

$0 |

$6,026,029 |

$10,563,082 |

$14,745,299 |

$12,904,912 |

$10,409,179 |

TOTAL EXPENSES |

$12,274,670 |

$8,455,894 |

$5,238,626 |

$3,757,139 |

|

|

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

--------------- |

|

--------------- |

--------------- |

--------------- |

--------------- |

||

|

EXCESS (DEFICIT) |

$3,174,097 |

$532,655 |

$554,113 |

$2,087,329 |

($654,755) |

($1,485,524) |

($233,323) |

$141,075 |

$1,633,625 |

EXCESS (DEFICIT) |

$363,013 |

($251,106) |

$505,791 |

$513,859 |

|

|

Tot 83 - 93 |

Tot 83 - 91 |

1993 |

1992 |

1991 |

1990 |

1989 |

1988 |

1987 |

1986 |

1985 |

1984 |

1983 |

Note: The excess shown from 1983 to 1993 is for $3,174,049 but that does not include 1992 expenses. Based on prior year expenses, an estimate of $2,500,000 in expenses for 1992 is not unreasonable, thus a more likely balance figure for the years 1983 to 1993 is an overall excess of $675,000.

| Table 4: Straight Foundation, Inc. 1985 - 1995 (below) gives a detailed breakdown of incomes and expenses for Straight Foundation, Inc. by year from 1985 to 1995, plus two total columns. One total is for the years 1985 to 1991 because it is a complete spread sheet. The other total is for 1985 - 1995 (not including expenses for 1992 and 1994). Straight Foundation, Inc. was transformed into present name and mission in 1985. I have its returns from 1985 through 1995 minus the 1992 and 1994 returns. The income-only for 1992 and 1994 are found on Schedule A to the 1995 return. Table 3 shows total income for the foundation through 1995 to be $ 7 million and total expenses to exceed $ 9 million resulting in an overall deficit of over $2 million. |

Table 4. Income & Expenses for Straight Foundation, Inc. 1985 - 1995

|

INCOME |

Tot 85 - 95 |

Tot 85 - 91 |

1995 |

1994 |

1993 |

1992 |

1991 |

1990 |

INCOME |

1989 |

1988 |

1987 |

1986 |

1985 |

|

|

donations & grants |

$2,269,933 |

$2,011,361 |

0 |

0 |

184,292 |

74,280 |

5,000 |

0 |

donations & grants |

0 |

0 |

145,508 |

843,992 |

1,016,861 |

|

|

rentals |

$4,354,800 |

$4,354,800 |

0 |

0 |

0 |

0 |

406,596 |

571,806 |

rentals |

604,848 |

619,848 |

590,748 |

780,477 |

780,477 |

|

|

interest |

$155,089 |

$96,810 |

18,889 |

22,840 |

10,848 |

5,702 |

474 |

1,041 |

interest |

14,303 |

13,900 |

17,600 |

23,337 |

26,155 |

|

|

land sale |

$8,927 |

$8,927 |

0 |

0 |

0 |

0 |

0 |

0 |

land sale |

0 |

0 |

0 |

0 |

8,927 |

|

|

settlement from law suit |

$20,000 |

$20,000 |

0 |

0 |

0 |

0 |

0 |

0 |

settlement from law suit |

0 |

20,000 |

0 |

0 |

0 |

|

|

program services |

$113,484 |

$0 |

0 |

0 |

113,484 |

0 |

0 |

0 |

gross receipts |

0 |

0 |

0 |

0 |

0 |

|

|

collected bad debts |

$5,131 |

$0 |

5,131 |

0 |

0 |

0 |

0 |

0 |

collected bad debts |

0 |

0 |

0 |

0 |

0 |

|

|

miscellaneous |

$52,272 |

$52,272 |

0 |

0 |

0 |

0 |

0 |

0 |

miscellaneous |

52,272 |

0 |

0 |

0 |

0 |

|

|

other |

$22,685 |

$22,685 |

0 |

0 |

0 |

0 |

0 |

0 |

other |

0 |

0 |

0 |

22,685 |

0 |

|

|

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

|||

|

TOTAL INCOME |

$7,002,321 |

$6,566,855 |

$24,020 |

$22,840 |

$308,624 |

$79,982 |

$412,070 |

$572,847 |

TOTAL INCOME |

$671,423 |

$653,748 |

$753,856 |

$1,670,491 |

$1,832,420 |

|

|

EXPENSES |

Tot 85 - 95 |

Tot 85 - 91 |

1995 |

1994 |

1993 |

1992 |

1991 |

1990 |

EXPENSES |

1989 |

1988 |

1987 |

1986 |

1985 |

|

|

grants to Straight, Inc. |

$3,280,747 |

$2,724,249 |

0 |

556,498 |

0 |

150,000 |

grants to Straight, Inc. |

534,817 |

0 |

242,421 |

541,292 |

1,255,719 |

|||

|

grants to others |

$58,000 |

$0 |

58,000 |

0 |

0 |

0 |

grants to others |

0 |

0 |

0 |

0 |

0 |

|||

|

accounting fees |

$66,582 |

$56,423 |

1,000 |

9,159 |

6,983 |

8,911 |

accounting fees |

7,821 |

4,946 |

5,641 |

13,800 |

8,321 |

|||

|

bookeeping fees |

$12,802 |

$0 |

0 |

12,802 |

0 |

0 |

bookeeping fees |

0 |

0 |

0 |

0 |

0 |

|||

|

legal fees |

$480,990 |

$473,871 |

424 |

6,695 |

4,120 |

10,990 |

legal fees |

46,670 |

277,013 |

22,084 |

100,125 |

12,869 |

|||

|

administrative expenses |

$15,537 |

$0 |

0 |

15,537 |

0 |

0 |

administrative expenses |

0 |

0 |

0 |

0 |

0 |

|||

|

telephone |

$5,703 |

$5,703 |

0 |

0 |

0 |

0 |

telephone |

0 |

0 |

0 |

4,208 |

1,495 |

|||

|

postage and shipping |

$6,058 |

$6,058 |

0 |

0 |

0 |

0 |

postage and shipping |

0 |

0 |

65 |

4,830 |

1,163 |

|||

|

travel |

$3,150 |

$3,150 |

0 |

0 |

0 |

0 |

travel |

0 |

3,150 |

0 |

0 |

0 |

|||

|

insurance |

$208,407 |

$195,505 |

5,775 |

7,127 |

58,926 |

28,520 |

insurance |

49,210 |

28,641 |

3,293 |

26,915 |

0 |

|||

|

rental expenses |

$4,358,938 |

$4,358,938 |

0 |

0 |

293,606 |

460,629 |

rental expenses |

528,232 |

1,495,300 |

549,589 |

544,452 |

487,130 |

|||

|

rent |

$511 |

$511 |

0 |

0 |

0 |

0 |

rent |

0 |

0 |

511 |

0 |

0 |

|||

|

office supplies |

$3,869 |

$3,518 |

351 |

0 |

0 |

0 |

office supplies |

0 |

0 |

0 |

0 |

3,518 |

|||

|

other |

$761 |

$518 |

0 |

243 |

0 |

0 |

other |

0 |

0 |

0 |

0 |

518 |

|||

|

write down of assets |

$57,280 |

$57,280 |

0 |

0 |

0 |

57,280 |

write down of assets |

0 |

0 |

0 |

0 |

0 |

|||

|

depreciation |

$114,942 |

$0 |

46,047 |

68,895 |

0 |

0 |

depreciation |

0 |

0 |

0 |

0 |

0 |

|||

|

1995 |

1994 |

1993 |

1992 |

1991 |

1990 |

YEAR |

1989 |

1988 |

1987 |

1986 |

1985 |

||||

|

miscellaneous |

$24,413 |

$24,413 |

0 |

0 |

5,258 |

8,118 |

miscellaneous |

10,018 |

1,005 |

14 |

0 |

0 |

|||

|

outside services |

$560,366 |

$29,881 |

0 |

0 |

0 |

1,940 |

outside services |

1,993 |

6,207 |

13,500 |

6,241 |

0 |

|||

|

client refunds |

$89,843 |

$0 |

0 |

89,843 |

0 |

0 |

client refunds |

0 |

0 |

0 |

0 |

0 |

|||

|

fundraising |

0 |

FUNDRAISING |

0 |

0 |

0 |

0 |

0 |

||||||||

|

salaries & taxes |

$1,722 |

$1,722 |

0 |

0 |

0 |

0 |

salaries & taxes |

0 |

0 |

1,722 |

0 |

0 |

|||

|

officers & directors |

$43,944 |

$43,944 |

0 |

0 |

0 |

0 |

officers & directors |

0 |

0 |

0 |

0 |

43,944 |

|||

|

other wages |

$207,642 |

$207,642 |

0 |

0 |

0 |

0 |

other wages |

0 |

0 |

0 |

180,370 |

27,272 |

|||

|

payroll taxes |

$19,533 |

$19,533 |

0 |

0 |

0 |

0 |

payroll taxes |

0 |

0 |

129 |

14,743 |

4,661 |

|||

|

advertising |

$4,429 |

$4,429 |

0 |

0 |

0 |

0 |

advertising |

0 |

0 |

0 |

4,429 |

0 |

|||

|

supplies |

$17,702 |

$17,702 |

0 |

0 |

0 |

0 |

supplies |

0 |

0 |

0 |

17,702 |

0 |

|||

|

printing |

$76,414 |

$76,414 |

0 |

0 |

0 |

0 |

printing |

0 |

0 |

0 |

32,942 |

43,472 |

|||

|

travel & meetings |

$66,906 |

$66,906 |

0 |

0 |

0 |

0 |

travel & meetings |

0 |

0 |

0 |

49,811 |

17,095 |

|||

|

outside services |

$2,350 |

$2,350 |

0 |

outside services |

0 |

0 |

0 |

2,350 |

|||||||

|

miscellaneous / other |

$15,911 |

$15,911 |

0 |

0 |

0 |

0 |

miscellaneous / other |

0 |

0 |

2,925 |

12,678 |

308 |

|||

|

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

|||

|

TOTAL EXPENSES |

$9,274,967 |

$8,396,571 |

$111,597 |

$766,799 |

$368,893 |

$726,388 |

TOTAL EXPENSES |

$1,178,761 |

$1,816,262 |

$841,894 |

$1,554,538 |

$1,909,835 |

|||

|

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

------------ |

|||

|

EXCESS (DEFICIT) |

($2,375,468) |

($1,829,716) |

($87,577) |

($458,175) |

$43,177 |

($153,541) |

EXCESS (DEFICIT) |

($507,338) |

($1,162,514) |

($88,038) |

$115,953 |

($77,415) |

|||

|

Total 85- 95 |

Tot 85 - 91 |

1995 |

1994 |

1993 |

1992 |

1991 |

1990 |

1989 |

1988 |

1987 |

1986 |

1985 |

Note: Expenses for 1992 and 1994 are not available. Based on other years, estimated combined expenses of $160,000 for 1992 and 1994 would not seem unreasonable which would result in an additional deficit of $58,000 = ($22,480 + $79,982).

|

Now that you have had a chance to look over the spread sheets, let's look at just what these incomes and expenses for the two Straight organizations include. Specific Assistance to People or White Kids-only Need Apply. An analysis of Straight’s tax returns shows that it grossed nearly $100,000,000 of which $18,000,000 alone was from tax exempt donations. I believe that, for the most part, the donors of the money were led to believe they were donating money to help teenagers receive drug rehabilitation, though some donors thought they were helping pay for Straight’s legal expenses in its numerous civil litigations and others felt they were helping the Straight building fund while still others felt they were educating the public about the dangers of improper drug use. But how much of the donated money actually went to help needy kids receive drug rehabilitation? Citizens and corporations donated $18 million, in large part, to help needy kids get the drug treatment that Straight claimed they needed, yet Straight’s own tax returns show that only $1,375,024 was used for specific assistance to people. In other words, Straight’s own records show that less than 8% of every dollar donated actually was used for assistance to needy people. Straight began operation in 1976. According to the Saint Petersburg Times a special report on Straight in 1978 called Special On-site Monitoring Report on Straight by Florida’s Bureau of Criminal Justice Planning and Assistance (BOCJPA)'s assistant chief John H. Dale, Jr. found that Straight ‘disguised’ client fees as ‘donations’. According to the Times article in those days Straight asked parents for donations, "but program officials have insisted that payment is not required." The report stated that Jim Hartz (then Straight’s clinical director) "could only remember one instance in which the fees had been waived." (About 450 people had been enrolled in Straight by then.) [Saint Petersburg Times, May 7, 1978, p. 3b.] Another finding of the BOCJPA report was that in its first 18 months of operation Straight had enrolled 450 youths but only one had been black. Could it have been that Pinellas County Florida had no drug problem with black youths? Well Operation PAR was another juvenile drug rehab program in Pinellas County then and Operation PAR had a population base which varied from 40 - 50 youths–ALL WERE BLACK. At its inception Straight had six young counselors who had graduated from The Seed (and who hopefully had graduated from high school), a clinical director who had been a parent in The Seed and was a high school dropout, and a director with a masters degree in clinical psychology. By comparison PAR counselors had to have at least two years of college. Straight had started with $100,000 in federal grants its first two years plus other private cash donations. The facility had been donated. Operation PAR was not grantless either. Operation PAR made a distinction between casual use of beer and marijuana, Straight does not. In 1981 Straight charged between $750 - $1,700 (it claimed based on a person’s ability to pay); PAR charged about $3 per session. [Saint Petersburg Times, March 3, 1978, p. 3a] In 1971 doctors Robert L. DuPont, Jr. and Richard Katon published an article in Modern Medicine in which they estimated that there were 17,000 presumed addicts in Washington, D.C. and that 91% were black.. [DuPont and Katon, "Physicians and the Heroin Addiction Epidemic", Modern Medicine (6-28-71), p. 123.] DuPont testified to Congress in 1971 that . . . opiate addiction is concentrated in the lower social classes. In Washington, D.C., only about 4 % of our patients [on methadone maintenance] are white . . . [U.S. Congress, House Select Committee on Crime, Narcotics Research, Rehabilitation, and Treatment, 92d Congress, 1st Session, 1971, Pt 1, p.157.] DuPont went on to become the White House Drug Czar, and, later, a paid consultant for Straight. In fact, he has testified in deposition that it was his idea for Straight to go national. With DuPont living in the Washington, DC area, and with his "expert knowledge of drug abuse in the black community" in the national capital area, it is not surprising that Straight opened a treatment facility in 1982 in the Washington, D.C. area to treat the drug problem that he knew blacks were having there. In February 1983 during deposition for the Fred Collins trial Dr. Miller Newton, Straight’s new director, stated, incredibly, that out of 156 kids at Straight–DC, he thought there were 4 blacks, 3-4 Hispanics, 1 oriental, and no native Americans. When asked by Mr. Collins’ attorney, And these [Straight] kids come from a higher economic background, do they not? Newton had replied, Mostly but not always. Speaking at a press conference in 1978 Straight’s then director Jim Hartz admitted that out of 200 clients currently enrolled at Straight-St Pete there were only three blacks and two other minorities. And yet five years later at the Fred Collin’s trial, Dr. Newton admitted that out of 260 some kids at Straight-St. Pete, there were no blacks! Six years later in 1989 Straight’s national research director Dr. Richard Schwartz published a NIDA funded study on Straight-DC titled Outcome of a Unique Youth Drug Abuse Program: A Follow-up Study of Clients of Straight, Inc. in which he described the race distribution in the demographic characteristics of the study sample of 222 follow-up clients as 99 whites and 1 black. In 1990 Lee County, Florida awarded a $10,000 grant to a juvenile drug rehab program which appeared to have many similarities to Straight called Outreach in Cape Coral, Florida. There was a stipulation that the money was to be used to help minorities who could not afford the program’s fees. Yet an expose in the Ft Myers News Press found that Outreach had no minority clients or minority staff members! In a sworn affidavit made by Straight Foundation board member and attorney Jay Snyder on January 17, 1991, Mr. Snyder made this statement, . . . research has shown that over the last 3 years there has been a decline in Straight’s market, to-wit: middle and upper income children involved in drugs. Instead, more lower income families are affected. The early Straight had been funded, in large part, by federal tax money. Some of that tax money had been paid by black citizens, yet Straight had not marketed to black teenagers. Then, suddenly, after six years of criticism by the government and by the media, Straight finally hired its first black, executive staff member. Her name was Beverly Hardy. She was hired to be trained to become the program coordinator for Straight--Cincinnati. And she had the perfect credentials to be a Straight program coordinator. She lacked a bachelor's degree from a four year college, but she did have an associate degree. She had a "nine-year drug past." And her degree had nothing to do with drug rehabilitation at all. It was an associate degree, appropriately, in marketing. Somebody got to the Saint Petersburg Independent (the old evening edition of the Saint Petersburg Times) which did a three day serial promotion on Straight. The series was written by a black female reporter named Bettinita Harris (we know this because her picture is included) and featured many stories including that of Beverly Hardy who is quoted as saying, I wish the word would get out that Straight doesn't have a color. The new ebony and ivory Straight had the series mimeographed and distributed as a promotional brochure. [Saint Petersburg Independent, 7-27-82, p. 1b; 7-28-82, p. 1b; 7-29-82, p. 1b]. In 1985 a newspaper reporter for the Richmond Times-Dispatch named Joy Winstead did a special three article report for the Sunday edition of that paper on Straight. She featured Family A and Family B–both had a child in Straight. In Family A the father was a manager with five years of college and the mother with one year of college. They had recently moved back from Europe. Their eldest daughter had been picked for a school for exceptional children because of her high IQ. She had studied piano, violin, gymnastics and dance. But this exceptional child had become involved in drugs which led her to having sex with several men, to committing crimes, to slicing her wrists, and to finally having a homosexual affair with an older lesbian woman! [Author: This is a typical scenario from Miller Newton's book Kids, Drugs and Sex.] Finally she found Straight and is maintaining a 3.5 average in high school! The father of Family B had five years of college and the mother two. Yet their son had become involved with drugs. One day the mother had noticed the boy had red eyes. That’s a good clue, Ms. Winstead had written. They like to blame it [red eyes] on the pool. Straight was so pleased with the article that they had it printed up and used as an eight page promotional brochure. The back page shows a table with statistics on Straight. One statistics states: The average [Straight] client comes from a middle-class suburban home (60 percent of the families have incomes over $40,000) and has an above-average IQ. Straight wasn’t saying that 60% of the nation’s drug using teenagers were now from upper-income, middle class families; Straight was saying that drug abusing kids can be found in ghettos and in affluent white neighborhoods. And Straight was saying that if you are affluent and your kid has red eyes then he is using drugs and will either kill himself or become a homosexual unless you get him into Straight! [Richmond Times-Dispatch, January 13, 1985] If you watched any of the 2000 GOP convention in Philadelphia you saw a sea of black and white faces on stage, but there were few blacks in the ranks of voting delegates out in the audience. So, according to political commentator John Young of the Waco Tribune Herald, the camera shots of the audience kept showing the same black faces over and over. Usually when you saw a picture of George Bush, Jr., he was backed by J. C. Watts, the black congressman form Oklahoma. If you see a photo of George Junior back home in Texas where he is governor, chances are you'll see black political activist Michael Williams of the Texas Railroad Commission. George Senior once made a TV commercial for Straight after receiving a quarter million dollars in donations from Straight co-founders Mel Sembler and Joseph Zappala, and he made the two U.S. ambassadors. Today Mel Sembler is finance chairman for the national GOP and his wife Betty, who is called Ambassadorable by Florida's Governor Jeb Bush, was Jeb's finance co-chairman when he ran for governor. After his unsuccessful bid for governor of Florida in 1994 Jeb Bush formed the non-profit Foundation for Florida's Future which employed two of his campaign aides. But a 1998 expose by Florida TV station WJXT on that charity reported that only 27% of the raised money actually went to programs with most going to administrative salaries for foundation employees. The one shining example of the foundation's work that Jeb likes to boast about is the foundation's effort to form the Charter School in Miami for underprivileged kids which he had established along with black political activist T. Willard Fair, President of the Greater Miami Urban League. After winning the 1998 gubernatorial election, Jeb appointed T. Williard Fair as a co-chairman of his inaugural committee. The WJXT report found that only $33,000 or just 2% of the foundation's raised money went to the Charter School (although the foundation did loan it $40,000). The foundation's annual report shows that the Sembler Company and the Huizenga Family Foundation both gave $5,000 or more to Jeb's foundation [former drug czar and paid Straight consultant Robert DuPont sits on the board of Psychemedics, a Huizenga's drug hair testing company.] In her continuing efforts to affect the nation's drug policy Mrs. Ambassadorable has formed a new tax exempt, anti-drug foundation called Save Our Society from Drugs or S.O.S. Prominent on its board of directors is none other than T. Williard Fair. Used to be in Pinellas County Florida that if you were a young black person with a real drug drug problem you went to Operation PAR, but if you were a white teenager who had drunk some beers or experimented with marijuana, or if you had a drug problem, you went to Straight. But today Betty Sembler is on the board of directors of Operation PAR! [Saint Petersburg Times, 7-14-95, p. 3b] Perhaps Straight felt it was not so important to accept minority clients or to hire minority staffers as long as it told state officials that it had an affirmative action policy. Whatever. The question remains: Is Straight’s motivation to help American youngsters?--as it claims. Or is it to help white American youngsters? Or is it simply to make money by marketing a product to the parents of white American youngsters-- they being better able to pay Straight’s huge fees than minority parents. Salaries. Straights’ biggest claimed expense, by far, is in salaries. All totaled the Straight’s claim to have paid out almost $43 million in salaries! People who were there might would question this statement. They know that Straight had no medical doctor salaries to pay. That unpaid old comers did most of the therapeutic work. That most of the professional staff were kid graduates who were paid minimum wage and that some of these were program graduates in training who were not paid a salary at all. There were Straight parents who were nurses who apparently donated time, and others paid services in kind. Volunteer parents manned the telephones and helped in other clerical duties for free, and they transported kids to medical doctors for free. They manned booths to collect donations and they gave talks to civic groups--all for free--to advertise Straight. Straight did not run dormitories so there were no beds to be made or meals to be cooked–at Straight’s expense. If any food was prepared, volunteer parents did the preparation. Major building improvement items were done by parents for free. You might be surprised to learn that, according to their records, apparently Straight did pay a lot of money in salaries as you can see from the following yearly salary statements dated July 1, 1991: 1991 Salaries Straight–Tampa Bay

These are just the salaries for Program Services and do not include salaries for corporate officers which we will look at momentarily. As you can see, Straight did have a large number of employees. If you were to tally up their yearly salaries the combined total would equal $3,040,422.60 (not including Straight--Virginia Beach). Straight–Virginia Beach is not included above because it had closed on or about February 9, 1991 under allegations of child abuse. (Straight--Southern California closed in August 1990 also under allegations of child abuse.) To compute the portioned salary for Straight–Virginia Beach in 1991, consider the following. Straight–Virginia Beach closed about 4 1/3 months into Straight’s fiscal year which began October 1, 1990. From client population data supplied as part of Exhibit A to an affidavit signed by Straight board member Jay Snyder on January 17, 1991 we can conclude that Straight--Virginia Beach closely corresponded in size to Straight-Detroit. Thus we can roughly use the total salary figure for all employees at Straight Detroit ($400,536.60) as a basis for Straight–Virginia Beach. Allowing 2 months for severance pay, one could compute salary at Straight-Virginia Beach to be 6.33/12 x $400,536.60 = $211,383.18. Thus one should be able to reasonably estimate that in 1991 Straight paid out $3,251,805.60 in wages paid to field employees ($3,251,805.60 = $3,040,422.60 + $211,383.18). But according to Straight’s tax return for 1991, Straight claimed to have paid out $3,823,120 for program services. That’s a difference of $571,314. How could Straight possibly account for that half million dollar discrepancy? Though only just a half million dollars, discrepancies like that over 10 years could amount to $5 million. Could it have been paid out in overtime or special pays? Look at the payroll statement for Straight–Washington for the two week period which was paid on April 7, 1987: DC payroll part 1, DC payroll part 2, DC payroll part 3, DC payroll part 4. Now look at the first blacked-out payee in payroll part 1. See the number 1461.54 below the blacked-out name. That’s the two week pay for this salaried employee who grossed $1,461.54. Now look at the third name. See the numbers 6.6000 2500 16500. This person earned $6.60 an hour and worked 25 hours for a gross pay of $165.00. Looking down the fourth column of numbers you can readily identify the hourly employees and the numbers of hours they reported in the 80 hour period: 25, 80, 80, 61.5, 37, 15, 80 . . . In all 14 out of 28 hourly employees worked less than a full 80 hours. Look at the fourth employee. That employee made $37.85 in overtime. In all, had all employees worked their full 80 hours, the payroll would have increased by more than $3,800, whereas overtime and special category pays accounted for just over $1,000 in payroll. Unfortunately I have only this one payroll from one center to analyze, but, according to this statement one would might assume that though Straight did sometimes pay overtime or special pays, it appears that the hours people worked less than 40 hours per week would indicate that this shortage outweighs overtime by 4 to 1. In other words an analysis of Straight's own data would indicate wages paid to field office personnel of about $3.25 million, not $3.82 million as declared in its tax returns. And while it is true that Straight could have paid out more than $3.25 million owing to overtime and special pays, the only evidence I have would say the opposite. It would say that Straight actually paid out less than $3.25 million, not more, owing to the fact that many workers did not work a full 80 hours. Now this is all based on one payroll from one center. It could be a fluke. Or maybe Straight will claim it gives out half a million dollars yearly in Christmas bonuses. Yet the doubt remains. So where did that half million dollars go and could there have been similar discrepancies in other years? In February 1991 Bernadine Braithwaite, then Straight’s national executive director, made an emotional, video-taped appeal to Straight parents for increased fund-raising efforts. Citing a 65% reduction in enrollments she made this statement: Straight has experienced a severe drain on its financial resources . . . In order for Straight to keep its remaining facilities operating we need the help of all our families in the area of client referrals and fund raising . . . I’ve restructured the organization, laid-off personnel, cut salaries at all levels . . . [Kim Keeler, Channel 13 Eye Witness News special serial report "Straight: Healing or Harming?", c. 1992] But whose salaries "at all levels" had she cut? Tax returns for the years 1990 and 1989 show that five months before she made the plea for additional fundraising efforts by the parents, her own salary had increased from the previous year from $132,000 to $145,200. Her last salary reported to the IRS five months before that broadcast showed an increase to $145,200. Her salary for 1991, the year she made the broadcast, increased even more to $151,417. In fact, in 1990, including contributions to employee benefit plans and her expense account, Mrs. Braithwaite’s share was $172,098. In the same period Page Perry’s salary increased from $72,000 to $86,400, Anthony Agliardi’s from $73,425 to $88,110. The fact is that all of the top five paid employees (other than officer’s, directors and trustees) received salary increases over the previous year putting them all at $50,000 or more. Additionally, the total number of "other" employees paid over $30,000 increased from 24 in 1989 to 30 in 1990. According to their tax returns, in 1990 the top five highest paid employees (other than officers, directors, and trustees) received a combined total in compensation, contributions to employee benefit plans, and expense accounts of $518,844 and 30 other employees received at least $900,000 in salaries alone. in 1990 Straight claimed 30 employees earning more than $30,000. One of the top 5 highest paid earned $50,000 even. So these 30 people earned anywhere from $30,001 to $49,999. Splitting the difference gives an average salary of $40,000 which results in $1,200,000 in salary. Using Straight’s benefit rate of 15.1% these other 30 employees probably would have made more like $1,381,200 in combined benefits and salaries and thus the top 35 paid employees received something like $1,900,044. In all Straight reported $8,677,568 in total wages and benefits for all employees in 1990. As we have seen, out of more than $18 million in tax exempt contributions, only 8% was used to actually help needy kids receive drug rehabilitation treatment. Out of all monies received, contributions plus revenues, Straight claimed to have paid out more than $44 million in wages and payroll taxes. So how much of that was used to actually treat kids? To answer that question, we need to look at Straight’s tax return for 1989 which shows salaries and wages for management and general to be $984,372. According to Straight's balance sheets for 1989 by CPA firm Grant Thornton--Straight's independent auditor--salaries for the corporate office totaled $984,372 for that year. Thus we know that when Straight reports wages and salaries for management and general on its income taxes, Straight includes management and general of the corporate offices only. That would mean that there are no management and general costs associated with the several treatment camps. If you look back at the 1991 Straight salaries by operating centers ( 1991 Salaries Straight–Tampa Bay for example), you will notice that while many of the field employees are dedicated to the clinical treatment program or program services (e.g. program counselors, clinical director, senior and junior staff), many others are involved in the management and administration of the camp (e.g. camp administrator, business manager, marketing rep, clerks, secretaries and receptionists. Straight--Atlanta had its own collections manager.) By my calculations, the administrative workload in the various treatment camps varies between 28% - 44% depending on what percentage of a secretary’s time or a clerk’s time one wants to attribute to administration vice program services. I will assume a safe 33 1/3% of salaries for the field operating offices to be for management/administration. According to Straight's 1991 tax return, Straight claimed the following salaries and wages: program services $3,823,120, management and general $1,088,843, fundraising $159,297. Well here’s the problem. Straight claimed $1,088,843 for the management of the program. But now we know that that figure only includes management and administration of the headquarters office. However, 1/3 the cost of operating the several treatment camps was also for management and general. So field operating salaries should have been reported, I believe, as: program services $2,548,720 and management $1,274,370. In other words, in 1991 Straight, by my analysis, should have reported the following: program services $2,548,720, management and general $2,363,213, fundraising $159,297. Thus Straight paid out $2.5 million for program services and $2.5 million in management and fundraising. This is significant because Straight was the recipient of CFC and United Way funds. If Straight reported to potential donors that 75% of every dollar donated went to treatment as is indicated on their 1991 tax form, that would not have been correct. A more realistic figure is just half of each dollar went to treatment. So only 8% of all money donated actually was used to aid deprived kids and only 50% of all money paid out in salaries was actually used for treatment (not including the equivalent of millions of dollars in donated time by parents who performed various administrative tasks for free.) Now one final thing needs to be said about salaries. You recall that in March 1978 Florida’s Bureau of Criminal Justice Planning and Assistance (BOCJPA) produced a special report on Straight which had received federal LEAA grants totaling $100,000 in its first two years of operation. The grant guidelines had clearly stated that the money was to be used for salaries only. Another finding of the report was that Straight founder Mel Sembler had violated federal conflict of interest regulations because the LEAA money had been granted for use for salaries only yet the money had been placed in a single bank account along with other Straight funds at First Bank of Treasure Island–a bank which included Mel Sembler among its corporate directors! The report further found that Straight officials Richard Batchelor, Helen Petermann, and Marlene Hauser had violated federal conflict of interest regulations because either they or a member of their family was receiving part of the grant money as salary. Now one might tend to forgive Straight for these mistakes (which is apparently just what BOCJPA did) because, after all, Straight was just a startup charity then. But you should also understand that the LEAA grants, which had been approved by BOCJPA, had been administered by the City of Saint Petersburg (that city and Pinellas County had also made grants to Straight). The significance is that one John White, Straight's treasurer, was a financial officer for the City of Saint Petersburg! [Saint Petersburg Times, March 3, 1978, p. 3a; March 19, p. 23; March 24, p 3b; May 7, 1978, p. 3b.] $1.3 Million in Miscellaneous Expenses. Look at Table 3 to see how detailed Straight, Inc. broke down its expense items. Originally I had not intended to use this detailed breakdown in the spread sheet for Straight, Inc., preferring to roll up minor items into some catchall category like "miscellaneous" or "other". Problem is, as you can see, Straight, Inc. and the foundation themselves itemized some expenses as "miscellaneous" and others as "other". For example in Table 3 you see that Straight, Inc. has categories for "miscellaneous (probably prizes) fundraising" and for "miscellaneous non-fundraising" while Straight Foundation, Inc. in Table 4 used categories for "miscellaneous non-fundraising" and "miscellaneous/other fundraising". In Table 2, which combines the incomes and expenses for Straight, Inc. and for Straight Foundation, Inc., I include a line item for "miscellaneous" which includes only the non-fundraising "miscellaneous" items for the two entities. Fundraising "miscellaneous/other" is included under prizes, while all other expense categories not specifically itemized are arbitrarily lumped together by me in a category I called "other". From Table 3 we see that Straight claimed $1.3 million for ‘miscellaneous’ expenses (which does not include "miscellaneous" expenses for 1992 as that data is unavailable. So look again at the detailed breakdown Straight, Inc. makes in Table 3. What could Straight have conceivably included under "miscellaneous". If that $1.3 million was not for rent, or salaries, or bad debt. Not for printing, nor travel, nor building maintenance. Nor for any of the other specified items. Then what was it for? How could Straight claim it spent $1,345,463 for "miscellaneous" items. Just where did that 1.3 million dollars go? Bad Debts. (Note: BAD DEBTS UNDER CONSTRUCTION) Straight, Inc. files its taxes on an accrual basis. This means that they report income from revenues based on what clients owe them–not on what was actually received. Client fees that are not collected are reported as 'bad debts'. For example, in 1991 Straight reported revenues of $4,743,445 which is what they claimed was owed to them for client fees. But they claimed that parents did not pay them $1,233,266 of the owed money. Thus $1,233,266 was reported as an expense item under the category ‘bad debts’ which is the proper way of reporting when using an accrual basis. Another way of looking at this is that Straight actually claims to have taken in just $3,510,179 in revenues in 1991 or the difference between the two. As you might expect "bad debts" work both ways. In 1992 Straight claimed $1,104,691 as income from "forgiveness of bad debts". Apparently this means that Straight had at some point itemized some expense(s) totaling $1,104,691 for some item(s) but the party(s) to whom the money was owed had excused Straight from paying it and therefore it had to be shown as income to offset the claim as an expense. So let’s look at this "bad debt" business. If somebody forgave Straight of $1 million dollars, do you think Straight, being a charity and all, might have forgiven any of its debtor parents? And who did Straight owe that $1 million dollars to who told them to just forget it? Most of the kids by far who entered Straight never graduated. Kids kept being placed back on first phase for silly rule infractions or never even made it off first phase, until sooner or later the parents caught on that no one realistically graduates under 1 or 2 years of treatment–regardless what they had been told upon intake, or they came to feel that Straight was harming kids or their own lives, or the kids turned of age and took themselves out of treatment or otherwise escaped, or state officials closed the Straights down for abusing children. But few realistically ever graduated. When a parent first placed a kid in Straight he was told that he would have to pay a substantial amount of money up-front and then so much a month. By 1989 the charge was $7,500 when you walked in the door. Few had that kind of money on-hand so emergency arrangements were made for second mortgages, loans against life insurance, loans from wealthy relatives. If you bought your kid in on Monday, gave them $5,000 cash and took him out on Tuesday because you learned he was being abused, Straight said the money belonged to them. And if you had not yet paid, the charity said that you owed them the $5,000. In 1989 the daughter of Mrs. Tempie Fortsom Worthy was discharged from Straight after a 38 day stay. Straight claims the little girl had been discharged because she had attacked a staff member and Straight does not tolerate violence from its clients. Straight sued the mother because she had not paid the full bill. Mrs. Worthy sued Straight for false imprisonment, physical and mental abuse, and for causing her daughter to be "frightened, humiliated, embarrassed and," caused to have "suffered severe physical pain and emotional anguish." Mrs Worthy waged a public campaign against Straight of demonstrations, mailings, etc. and Straight used money from the parents to apparently sue Mrs. Worthy again to silence her. [Tarrant County, Texas District Court, cause no. 96-129277-90] Service, Medical and Outside services. UFrom 1983 to 1995 the two Straights paid $113,038 in service contracts which includes such things as janitorial services (though much of the janitorial work was performed by kids and their parents). U$314,095 was claimed for medical services–though it is impossible to determine the true figure for medical services because Straight often combined apples and oranges. For example in 1985 $627,473 was reported for the absurd line item ‘food and medical’. What does this mean? $600,000 for medical and $27,473 for food, or $473 for medical and $627,000 for food? U The Straights claimed to have spent $2.3 million on outside services, but what does that mean? In 1988, for example, Straight, Inc. showed $266,970 for outside services. On the Schedule A Straight was required to list the five highest paid professionals it had engaged for ‘Professional Services.’ Straight listed $82,569 to Richard Milburn High School in northern Virginia for educational testing and tutoring services, and $32,500 to Rockville, Maryland psychiatrist Peter Cohen for medical services. Straight submitted that there were no others paid more than $30,000. That totals to just $115,069. So what was the other $151,901 in 1988 for outside services for? And so it can be asked fro the other years. Printing. Many Straight parents with special skills and abilities donated their services to Straight. One of these was Straight Foundation-Northern Virginia board member Dave Arrington who owned and operated a professional printing company in Manassas, Virginia. In addition to some apparently gratis work done by Mr. Arrington, Straight reported $1.3 million in printing costs. Awards and prizes. The Straights claimed to have paid out $3.5 million in awards and prizes. To get an idea of what this could entail, look at the Straight-Greater Washington’s fundraising budget for September 1, 1988 to September 30, 1989. Most projects entailed some costs–$10,000 for Christmas trees to earn $10,000; $10,000 in Super Bowl tickets to earn $20,000; $20,000 for an automobile raffle to earn $20,000. But many do not: donated time for a work-a-thon to earn $15,000; $2,000 from yard sales; $3,000 from craft shows; $12,000 on food re-sales back to parents; $10,000 from pew collections; $3,000 from newspaper recycling. Marketing. Include Clews. Grants. In 1985 Straight, Inc. changed its mission to one of educating the public on the dangers of adolescent drug abuse and changed its name to Straight Foundation, Inc. According to its 1985 tax return, at the beginning of the year the foundation had fund balances or net worth of $3,707,788. The people and organizations which had been led to believe they had raised that money to either treat kids at Straight or perhaps to pay for Straight’s legal expenses for having abused some kids, had been mislead. The new purpose of that money, as stated in the foundation’s 1985 tax return would be to "support and finance programs dealing with drug abuse education, prevention, control, treatment and rehabilitation." In 1989's return the state read "all income received is used to provide funding to organizations that address drug prevention, awareness and/or treatment in the adolescent community." In fact similar statements were made in all years from 1985 to 1993. The parents and organizations had, for the most part, raised money believing it would be used for Straight specifically. The money they thought they had raised to run Straight and to help needy kids receive Straight treatment could now be used for non-Straight treatment programs and even public awareness programs. This is not to say that these are not also worthy charitable causes. It is just to say that it is not what the people thought they were raising money for. And the wording in the IRS 990s and in the articles of incorporation are very important because if the 990 statements and the articles of incorporation stated that the purpose of the foundation was to aid Straight, Inc. specifically, then a case could be made that the foundation was merely a shell corporation setup to protect the members from personal liability and criminal involvement in the growing number of civil suits being waged against Straight and in the criminal investigations being conducted against Straight. On the other hand, if the articles and the 990s did not mention Straight specifically, then the people who had donated the money to help needy kids get treatment at Straight or to help Straight pay its court loses, had been mislead. Straight, Inc., a new treatment program for adolescents, was then created. It had no assets. The foundation had the property and rented it back to Straight, Inc. In 1985 Straight, Inc. paid the foundation $780,477 in rent. But the foundation, in all its magnanimity, made a grant to Straight, Inc. for $1,255,719 to operate. In all the foundation would make $3,280,747 in grants to Straight, Inc. from 1985 to 1993. (In each year in which grants were made, Straight, Inc. was named as the recipient except for a $534,817 grant made in 1989 and a $150,000 grant made in 1990 where in each case no specific receiver is named. I assume both were made to Straight, Inc.) In the combined income and expenses of Table 3 I do not show the internal grants as it is a wash. The logical question to ask now is, "Why didn’t Straight, Inc. keep its raised money, and just form a new organization called Straight Foundation, Inc.?" Combining Categories. Sometimes Straight, Inc. would combine two completely unrelated items like food and medicine. For example, in 1984 food and medicine were listed as separate line items, but they were combined in 1985 for a total of $627,473 for the item "food and medical". What does this mean? $600,000 for medical and $27,473 for food, or $473 for medical and $627,000 for food? In cases like this I arbitrarily used a percentage from a neighboring year. In this case 96% of the total from 1984 for food and medical was for food and that is the percentage I used for 1985. Another example would be Straight's 1984 reporting of "supplies and postage" as a combined item even though the IRS form clearly form asks for separate line items for each. In this case I used the percentages from the 1983 return to attempt to determine the actual values for each. Property and Real Estate Holdings or Turning a Million Dollar Investment into $80K. See Real Estate. Piercing the corporate veil. See Piercing the Corporate Veil. Summary: the 100 Million Dollar

Triangle.

The Straights had a stated

combine |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}